I really really want to be debt free in 18 months, I had wanted it to be one year but I can’t realistically do that with my income. I have some medical bills and a couple credit cards that I want all paid off. Our mortgage will be paid off in two years and I would like to semi-retire then but the only way is to have everything paid off so I am aiming for 18 months, hopefully, it will be sooner than that then I can apply the extra to the house.

Please join me if you are also wanting to be debt free or just want to get your saving built up.

In order to do this, there are a few things you need to keep in mind and do.I will post at least once a month if not more on my progress.

1. Mindset is everything, You have to really want to do this. There will sacrifices required.

2. Attitude, You have to have the right attitude, you know this is what you want to do and you are going to do what it takes. you are going to be proud of the sacrifices you make and not feel deprived because you are doing without.

3. Be realistic, Set a realistic goal don’t try and be out of debt in a year when even if you put every penny you made towards it it would still not be paid off in a year.

4. Set goals, set smaller goals to help you obtain your larger goal. ( such as making your own bread instead of buying it.)

5. Challenge yourself, One thing I do is I try to be as cheap frugal as I can and I take great pride in it. I let my family and friends know that I am trying to be as cheap frugal as I can and take great pride when I can show them where and how I have saved money. Some are pretty extreme so now I really like the shock factor of they can’t believe I do that.

And most of all remember it will not happen overnight, you didn’t accumulate it overnight it won’t go away overnight.

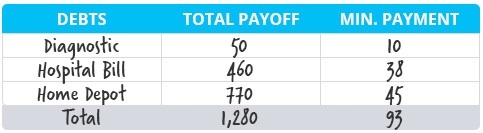

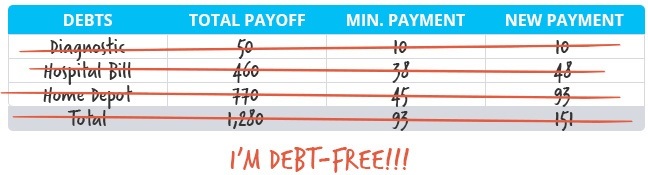

So the first thing to do is make a list of ALL your debt and expenses.

Start with your set monthly expenses, mortgage/rent, car payment, insurance, etc.

Next add up all your other monthly expenses, cable, gym membership, other memberships, utilities, phone, groceries, try to add in a little for deep pantry/ food storage, gas, personal loans, etc. Figure high.

Now add up all your other monthly minimum payments on your debt, medical, credit cards, etc.

Now add up how much you spend on all other things like eating out, coffee, snacks, all the little things that you don’t really think about.

If you have yearly or quarterly payment find the yearly amount then divide by 12 and put this back every month so when it is due you have it.

Now add all your income hopefully it is a little larger then your expenses, but if not not all is lost it can be done. (We will cover that in a bit. ) Figure low.

Now comes the fun part, and the part that you have to determine how dedicated you are to getting out of debt. Start looking where you can cut expenses. ( don’t be unrealistic if you know there is no way you are not going to do without your daily soda or coffee add it in. But also remember your goal is to get out of debt).What can you do to cut the utilities, the groceries, can you do without cable,?

Now set a tentative budget.Make it doable.

Put in all you set expenses including minimum credit and loan payments’ Insurance.

Add your utilities, groceries and other expenses subtract this from your monthly income. What you have left is the extra that you are going to apply to your debt using the Dave Ramsey snowball method.Here is an example from his site of how it works.

What Is the Debt Snowball Method?

When you begin Baby Step 2, you’ll start working on your debt snowball. This means you’re current on all your bills and have $1,000 saved in a starter emergency fund. The debt snowball method helps you stay motivated while paying off your debt by starting with the smallest debt and working your way up to the largest.

But wait. Doesn’t it make sense mathematically to pay on the debt with the highest interest rate first? Wouldn’t that save you the most money?

Maybe. But if you begin with the biggest one, you might think you’re not making fast enough progress, lose steam, and quit before you even get close to finishing. It’s important to pay your debts in a way that keeps you motivated until you’ve wiped them all out. Those quick wins will pump you up!

And that happens when you start with the smallest debt. Once you’ve saved your $1,000 starter emergency fund, list all your debts (except the house) smallest to largest. Now it’s time to get rid of them ASAP with the debt snowball.

Here’s How the Debt Snowball Works

Step 1: List your debts from smallest to largest.

Step 2: Make minimum payments on all debts except the smallest—throw as much money as you can at that one. Once that debt is gone, take its payment and apply it to the next smallest deb

t while continuing to make minimum payments on the rest.

Step 3: Repeat this method as you plow your way through debt. The more you pay off, the more your freed-up money grows—like a snowball rolling downhill.

First, If you are not current on your bills you will use all the extra you can to get current.

Then second, we are going to apply all the extra we have till we get a 1000 dollar emergency fund built. (To only be used in a true emergency.)

Then we will start on our debt. Have your set amount that you will apply every month if you have any extra leftover apply that to your debt also. ( if your electric bill was 20 less then you had budgeted apply that 20 dollars towards your snowball payment)

You can use this idea to help track your progress. Get a piece of paper and make a graph ( I just use a piece of lined paper) then mark it off so each lines equals 50 or 100 dollars till you have your desired debt free amount ( add your 1000 dollar emergency fund to this) then every time you pay off that amount color in a line when you are all paid off the graph will be all colored in, this way you can see what you have accomplished. You can do it all one color or have a separate color for each debt, or just make a rainbow however you want it .

I will be sharing some of the things I do and how to do them to save. The first thing you can do is go to 201 ways to save money, some of them are extreme it will depend on how much effort you want to apply to getting out of debt as I said some a pretty extreme and just not doable for some which is fine just do what you can, every little bit helps.

I am going to try and do a post at least once a week with frugal tips and ideas.

If you figured all your bills and income and you didn’t have enough income to cover all the bills you are going to have to get extreme and creative. Go to 201 ways to save for ideas. And start finding things to cut out. Call your creditors and see if they will lower the monthly payment or lower the interest rate it is worth a try the worst that can happen is they say no. If you have a choice of utilities call around and get the best rate. trade in for a less expensive vehicle, walk or use public transportation if that is an option, make use of the library for movies and books, Remember every dollar you save is a dollar towards getting debt free. Think about a part-time job or cleaning a house or two on the side even doing daycare even if it is only one child. Once again every little bit helps.

So are you ready to join me as I start down the road to be debt free? The sacrifices will be so worth it in the end when you don’t have to stress every month worrying about all the bills and that if something happens you won’t be able to pay everything.

You will so do this! Big party when you get to write your last check 🙂 We’ll be here cheering you on!!!

Lady Locust,

Thanks, It will feel so good when it is done. I have a couple friends doing this also so I think it will help being able to support each other.

Hope you had a wonderful Christmas. 🙂

Connie

Ranchers Wife

I’ve been doing this exact thing for about 15 months now, down to one CC with about $5K on it, paid off over $21K so far and keep plugging away, Yes I had a GREAT time for a while, then I woke up and slapped myself upside the head with a rock.

I would add to make sure you add a monthly cost for things like yearly Property Taxes, etc. I set $,xyz away each month in a separate envelope (locked in a safe, NOT in the bank) for when the bill hits, than pay it immediately so not tempted to use that on something else.

As far as doing things cheap? I refuse to “eat out” anymore, for the cost of one meal at the overpriced restaurants one can cook for several days, and a Brew at a Bar is $5-$6 bucks….. Absolutely NUTS! FYI, I have yet to run the furnaces this year, Wood Stoves are a GREAT thing, and I HATE buying Propane, wood is cheap and heats one’s self several times in the process hehehehe

NRP,

We have a separate account that we use for the once a year stuff, we have a small rental and we put that money back for that kind of stuff so we don’t have to worry about something sneaking up on us.

I hate to eat out I was a waitress for way too long I know what goes on in the back, Only one restaurant that I ever worked out was super clean in fact you could eat off the floor and that was one in Farmington ( TJ’s) don’t know if it is still that way since Jim is gone. So that and the high prices I just can’t do it very often, plus where we live it is too far to run to town just to eat lol.

Since we are going to the stock show we had to light the heater in the house haven’t had it on in over 4 years, it does still work lol. but when we put down new floors we covered most of the vents left just enough to keep the house from freezing if we need it.I to hate buying propane and I love my wood heat.

Praying you on to be debt free. Great post with how to accomplish this.

Maree Dee,

Thanks, I really hope to get this done.